Taking an Inventory of Investor Worries

The Pacifica Partners Winter 2016 Quarterly Commentary:

Most years, financial markets tend to rally in the month of December. As the 2015 holiday season wound down, investors found that Santa had deprived them of their traditional yearend rally. Instead of a rally, investors were left showered with volatility to close off 2015 and clinging to hopes that 2016 would start off better than 2015 ended. Thus far in 2016, investors have been sorely disappointed as global equity markets are off to their worst start in history after being down 6-10% already. This month’s newsletter looks at the issues that are causing investors so much concern and trying to highlight why so many are worried about the possibility of a recession.

Worries Topping the List

The biggest surprise of the economic recovery since the last recession is that seven years into it, economic growth is still subdued and halting. To put this in perspective, it is worth first noting that the US has the world’s fastest growing developed nation economy. In terms of momentum, it is the unmatched leader. In normal times, one would think that based on those descriptions, the economy would be booming. In fact, the US economy is about to set a dubious record of sorts: Never before in history has US real (inflation adjusted) economic growth stayed below 3% and nominal (non-inflation adjusted) growth remained below 5% for 10 years in a row. This year the consensus for 2016 US economic growth can be summed as “more of the same” with the economy expected to churn out 2-2.5% of economic growth yet again.

Accounting firm PwC recently came out with its annual survey of US CEOs which shows that only 27% of them believe economic growth will improve in 2016 and 23% believe it will decline. More importantly, only 35% believe that their revenues will increase. They are hardly a confident bunch.

Yet as gloomy as this might seem, the facts say “it’s not so bad”. In his 2016 State of the Union speech, President Obama stated “…the United States of America, right now, has the strongest, most durable economy in the world. We’re in the middle of the longest streak of private-sector job creation in history. More than 14 million new jobs; the strongest two years of job growth since the ‘90s…And we’ve done all this while cutting our deficits by almost three-quarters”. He might also have mentioned the record year in car sales with the US auto industry achieving nearly 20 million vehicles sold. For comparison, the previous peak was 17.4 million units–reached prior to the last recession.

Auto Sector In High Gear

The outlook for auto sales is positive as the age of the US car fleet continues to remain above average as consumers have been reluctant to replace their aging cars. At this point, with an unemployment rate of only 5%, interest rates still low by most any measure, the US economy should continue to see a strong contribution from the auto sector. However, if we look at the selling pressure in auto and auto parts stocks, it is clear that fear is prevalent as investors are wondering if we have seen the peak in car sales. Both Ford and GM have made significant moves to reflect their confidence in their outlook. Management of Ford has announced a special $1billion dividend payment to shareholders and GM just announced an increase in its dividend and stock buyback.

The US auto industry is a key pillar of the US economy. In a study published last year, the Center for Automotive Research determined that more than 1.5 million individuals are employed by the auto industry and over 5 million people in related sectors. For the government, the same study found that these employees earn nearly $500 billion annually in compensation and $65 billion in tax revenues.

The US auto industry is a key pillar of the US economy. In a study published last year, the Center for Automotive Research determined that more than 1.5 million individuals are employed by the auto industry and over 5 million people in related sectors. For the government, the same study found that these employees earn nearly $500 billion annually in compensation and $65 billion in tax revenues.

Outlook for Canadian Equities

Historically it has been the case that a strong US auto sector helped to underpin economic growth in other countries – especially Canada. However, this has changed in recent years as an increasing amount of production has been going to other countries such as Mexico and production that has been brought back to North America from developing nations has largely gone to the US and Mexico. Of all the investment dollars that have gone into the industry since the last recession, less than 1% has come to Canada. This is one of the reasons that the low Canadian dollar has not been able to translate into better economic growth for Canada. In short, Canadian manufacturing is not what it once was. This can be seen by the fact that Canada only received 0.20% ($118 million) of the $24 billion spent on automotive plant investment. Clearly, not a signal of confidence for Canada’s industrial future and clearly investment dollars are not trying to take advantage of the low Canadian dollar. Canada is now the smallest producer of autos in North America – having being surpassed by Mexico in 2014.

At this point, the collapse in oil prices and the mediocre level of economic growth in the US means that the Canadian export picture will be slow to improve. On top of that, the Canadian consumer is massively in debt but has begun the slow process of trying to repair the balance sheet and pay down debt. All of this means less money left for consumer spending to help propel the economy forward. At the risk of stating the obvious, there is not a lot underpinning Canada’s economic fundamentals – leaving the Canadian dollar about where it should be valued after its nearly 40% decline relative to the US dollar.

However, this does not mean that 2016 has no chance of yielding decent opportunities for Canadian equities. Studies show that equity markets and economic growth are not particularly well correlated. Instead, we believe that Canadian equities are under owned by many Canadian institutions and foreign investors. If the sentiment changes towards Canada, a trickle of capital could turn into a tidal wave into Canadian equities.

US Interest Rates

The US is also the only nation whose central bank has begun raising interest rates. There is considerable debate as to whether this is premature and there are those who say that the US should have been raising interest rates at least a year ago. From our perspective, the timing is better late than never. We believe that the waiting game related to the “Will they or won’t they?” aspect to the interest rate decision made investors single-mindedly focused on this at the expense of ignoring market fundamentals – not to mention the complacency that had crept into the markets.

The strength of the US economy has finally afforded the Federal Reserve the cover to begin to raise interest rates. Historically, after the first interest rate increase – markets suffer a period of volatility and eventually they begin to recognize that the economy has righted itself and the interest increases are a sign of strength. While this time could be no different – there are some problems that are causing the markets a certain level of anxiety.

In order to get a better level of insight into the economy, it is probably best to dissect it into a domestic side and an export oriented side. The domestic economy driven by consumer spending is strong and underpinned by improving wage growth and low unemployment. Government spending has begun to make a positive contribution to economic growth after years of spending restraint by governments focused on bringing in budget deficits. On the flip side, business investment is still largely stagnant and made worse by a rapid decline in spending in energy and mining.

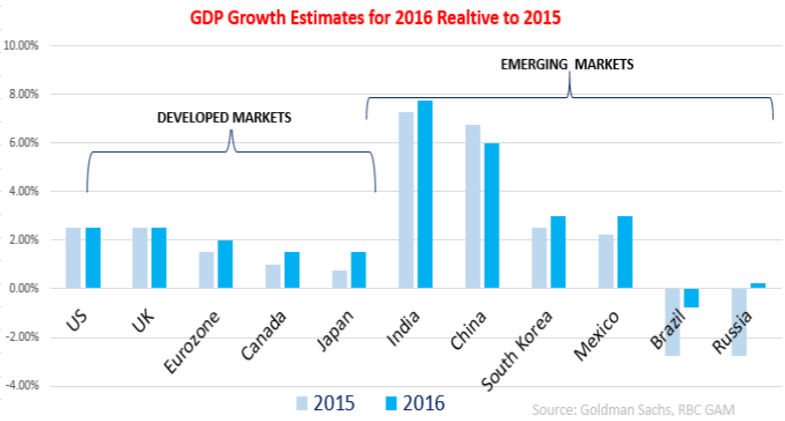

The export side of the US economy is being buffeted by the headwinds of a strong US dollar and slowing economic growth in the emerging markets – along with a European economy that is mending itself – albeit at a slow and steady pace. The chart on page 2 shows the economic forecasts for 2016 are for a replay of 2015.

China and the Emerging Markets

Of the developed nation economies, the US and the UK are showing the greatest strength while the rest of the world has seen better days. The downturn in the emerging markets has become one of the central issues for the markets. Brazil is seeing the worst economic growth since the Great Depression – along with massive debt and political problems centered on corruption extending all the way up to its President; Russia’s economy is in recession and inflation is near 12% as it deals with economic sanctions and a collapse in oil prices; India remains the lone source of optimism for the emerging markets but even there – the government has been able to produce only mixed results on its reform efforts. But China is of particular concern given that it is now the second largest economy in the world.

In our Q2 2015 newsletter, we had noted that since 2008, China was responsible for incurring nearly half of the world’s increase in debt. Looked at from another perspective, China’s debt has risen from $7 trillion in 2007 to about $30 trillion. It’s debt level is almost 3x the size of its GDP – much higher than that of the US. If that was not worrisome enough, half of all of the loans in the country are linked to its real estate market which has slowed. While the government has the money by most estimates to bail out the financial system, the cost will be large.

Despite the monumental debt increase, the Chinese economy is losing momentum. The Chinese leadership knows it must tackle the problems that threaten to bring down the entire system if the problems are allowed to fester. Many of the problems with the Chinese economy that we have highlighted over the years are now seemingly front page news. Specifically, China is trying to fight corruption; deal with inefficient “zombie” state owned enterprises and reduce the reliance of the economy on real estate, construction and capital spending on factories and infrastructure.

The Chinese authorities have been trying to nudge the economy into a more consumption driven model where consumer spending begins to take an increasing role in the economy. They simply have no other choice. The country is overbuilt to the point that the world has never seen anything like it. For example, the country has built up so much manufacturing capacity to the point that only 50% of it is being used. For comparison, even during a recession in the US, capacity utilization is about 70%. In order to begin productively using this excess capacity and put people to work, the country would have to begin growing by perhaps 10% or more. For perspective, the Chinese government data shows it is growing at 7% – a figure that is widely scoffed at and many estimates from economists have it as more likely to be 3-4%.

Investors have lost confidence in China and its leadership’s ability to steer the ship in the direction of its own choosing. No longer is the central government able to summon up 7-10% economic growth rates and paper over the problems that come from a pseudo-command economy. The Chinese economic experiment is about over and the government has a tiger by the tail as it tries to steer a new course. One potential silver lining in the cloud is that services make up about 50% of the Chinese economy—showing that the reforms are making their way through a long and arduous process.

Oil, Petro Dollars & Commodity Exporters

About twenty years ago, weak oil prices used to be seen as an economic positive because it meant that the US consumer (the single most important economic actor in the world) would get what amounted to a tax cut since it meant consumers would have to spend less money on fuel. However, consumers have channeled the savings from lower energy costs into savings and debt reduction. The longer the low prices persist however, the more consumers will come to believe low prices are here to stay and eventually they will begin to spend. While this is great news for the US economy—and any large energy consuming economy—the oil producing nations are hurting.

During the boom years, many of the oil producing countries such as Russia and the Middle Eastern OPEC members accumulated hundreds of billions of so-called “petro dollars” (dollars accumulated by oil exporting countries). They were able to invest these reserves all over the world in assets such as stocks, bonds, gold and real estate.

The collapse in oil prices has reduced the flow of petrodollars from about $700 billion in 2013 to less than $200 billion by the end of 2015. This means there is about $500 billion less flowing into financial markets and other investments. In addition to the lack of new money flowing into the financial markets, some countries are being forced to liquidate their assets to help meet the needs of their national budgets. This is amplifying volatility in the financial markets as these nations have transitioned from large buyers to large sellers. For example, analysts estimate Saudi Arabia has sold off about $80 billion in assets in the last year and China saw its reserves fall by $500 billion.

The chief exports of many emerging market countries are commodities. As commodity prices continue to spiral lower, it is feared that these countries will face significant headwinds since their economies will be growing slower and earning less income. Last year saw about $500 billion in outflows from these countries according to the International Institute of Finance.

Already, creditors have begun charging companies based in these countries higher rates of interest to reflect their perception of greater risk. Thus, these nations are being book-ended by falling economic growth and higher borrowing costs. But unlike prior eras when these conditions arose, many emerging market countries have the capacity to weather the storm for longer than many might think.

Markets Are Making Adjustments

It is likely that the US will have to continue to shoulder the lion’s share of the burden for global economic growth. Our Q3 2015 newsletter titled “US Consumer: Riding to the Rescue Again” stated that the US consumer side of the economy would be one of the few economic bright spots. As 2016 begins, we believe we underestimated how important the US consumer spending story would be. With the luxury of some additional time and data, it is much more in focus.

Analysts are busy trimming corporate earnings estimates and their targets for what they expect from the equity markets this year. We have been of the opinion that for far too long, the markets have looked the other way with respect to the fact that too few companies are able to grow their revenue. In recent months, this seems to be less and less so.

We are also seeing strong value in other parts of the world – especially Europe where earnings growth could substantially outpace US earnings growth. Part of this is due to the fact that European countries are able to get a tailwind from the weak Euro and the worst of government austerity could be behind us. Despite the negative headwinds, we believe that it is possible that emerging markets at some point this year will prove to be attractive markets for longer term returns.![]()

This report is for information purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. The information contained in this report has been compiled from sources we believe to be reliable, however, we make no guarantee, representation or warranty, expressed or implied, as to such information’s accuracy or completeness. All opinions and estimates contained in this report, whether or not our own, are based on assumptions we believe to be reasonable as of the date of the report and are subject to change without notice. Past performance is not indicative of future performance. Please note that, as at the date of this report, our firm may hold positions in some of the companies mentioned.

Social Media: It is Pacifica Partners Inc.’s policy not to respond via online and social media outlets to questions or comments directed to it or in response to its online and social media publications. Pacifica Partners Inc. does not acknowledge or encourage testimonials posted by third party individuals. Third party users that have bookmarked Pacifica Partners Inc.’s social media publications or profile through options including “like”, “follow”, or similar bookmarking variations are not and should not be viewed as endorsement of Pacifica Partners Inc., its services, or future or past investment performance. Copyright (C) 2016

© 2016 Pacifica Partners Inc. All rights reserved.