Productivity To the Rescue

In This Issue:

- US undergoing productivity boom while economy begins to accelerate

- Labor markets stabilizing

- Canada’s productivity gap & population trap

- Productivity booms raise wages & hold back inflation

For most industrialized nations, their respective economies fared better than expected in 2025. The shock of the trade and tariff dispute of early 2025 did not cause the sharp economic slowdown that economists had feared. Much like in 2020—following the global shutdown caused by the COVID pandemic—and despite rising interest rates and inflationary pressures, the global economy once again demonstrated notable resilience.

As tariffs rose sharply in the early months of last year and investment flows fell sharply, stock markets sold off sharply with most major stock market indices falling 15-25% in a six-week wave of panic induced selling. As the US walked back some of its tariff threats and trade deals were reached with many nations, the focus of the financial markets shifted towards standard issues such as the expected level of economic growth, inflation and in particular – the labor market. The labor market has been of particular concern for over a year as investors try to look through the murkiness of economic data and forecasts for any signal that there is an economic slowdown brewing or even any indication of a potential recession.

The US economy added only 584,000 jobs in all of 2025, the weakest annual gain since 2020 and the second weakest since the Global Financial Crisis that began in 2008. Monthly job creation averaged only 49,000 jobs per month – a nearly 70% decline from the 168,000 jobs created per month in 2024. However, one significant factor behind weak total job growth in the US is the fact that the civilian federal employee headcount finished 2025 lower by 9.1% which is equivalent to approximately 275,000 jobs.

In contrast, Canada’s federal civilian workforce has grown by nearly 40% over the past decade, peaking in the 2023–2024 fiscal year. Notably, the expansion of the federal workforce has been roughly double the growth rate of the Canadian private sector.

A reduction in the Canadian government’s federal civilian payroll is coming as Canada – like most nations – faces a severe fiscal crunch that has brought about rising budget deficits. The deficits of the last decade have doubled Canada’s national debt to $1.2 trillion with not much capacity left to raise taxes so spending cuts are going to have to be significant. With federal government payroll spending up nearly 83% in a decade, the government has begun downsizing its payroll. Apart from helping Canada to lower its federal budget deficit, the reduction in government payroll numbers should help to expand the labor supply as many businesses had been complaining of a lack of skilled labor. Budget cuts are aiming to reduce $60 billion from current expenditures with reductions in management and front line staff announced.

A closer look at the US labor market shows that while unemployment is still low as it ended at 4.4% in December 2025, the labor force barely expanded which is indicative of a soft jobs market and that means there is some slack in the labor market. Economists are wrestling with the data to discern if the US economy might be weaker than it appears. This comes about because as workers are discouraged from looking for work due to low expectations of finding a job, they often will decide to not look for work actively. Under such a scenario, the unemployment rate would mask economic weakness since workers who give up on looking for work are not counted as part of the labor force and therefore do not show up in headline unemployment numbers. But the labor market in the US is showing signals of bottoming out. Layoffs are easing and jobless claims are declining to levels consistent with a stable labor market.

US Economic Growth

While the final GDP growth figures for the fourth quarter of last year are yet to be published, estimates from the Atlanta Federal Reserve’s GDP Now forecast have been revised up to 5.4% from 2.7%. This is a stunning revision given the consensus amongst economists early last year was for a potential recession in 2025. A closer look at the factors behind the surge in U.S. economic activity shows that not only is growth strong, but the underlying quality of that growth is also high.

The data shows that one of the factors that fueled the sharp upturn in economic growth of the US was a sharp decline in the trade deficit. The trade deficit in October was down to $29.4 billion – down from $48.1 billion in the month before. Furthermore, US government data shows the October deficit number was the lowest since June 2009. Often times, an economy with falling income or slowing economic growth will show a falling level of imports. But for the US, it was the best of all worlds as imports fell last October by $11 billion and exports rose by $7.8 billion. In short, last October’s trade data contributed to an $18.8 billion improvement in the trade deficit and therefore helped to contribute to the sharp rise in expectations for US economic growth.

There is, however, a risk that the trade deficit could widen again in subsequent months given the US economy is strongly consumption driven and is posting the strongest economic growth amongst the developed economies. Higher GDP tends to coincide with rising imports. Meanwhile, exports will be dependent upon the level of economic growth in Europe and Asia. Thus, it remains to be seen whether imports will surge again or exports weaken due to lower demand for US goods.

The Productivity Surprise

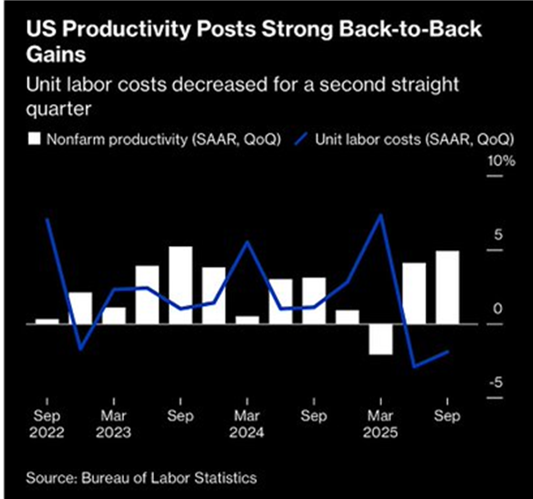

Financial markets have been disappointed that the stronger than expected US economy has not been reflected in the labor market. As noted above, job growth has been lukewarm. Gone unnoticed is that the US economy has been undergoing a productivity momentum burst . As the figure at the top of page 3 shows, the third quarter of last year saw US labor productivity growth move sharply higher by 4.9% – this was after second quarter productivity was revised higher to 4.1%. This data is pointing to a structural shift in the US economy’s ability to provide economic output with rising efficiency.

An economy’s productivity measures the amount of economic output produced per unit of input of labor and capital. A highly productive economy is able to produce more economic output (GDP) with less inflationary pressure. In other words, it is the best of all worlds when an economy can grow faster through efficiency.

Productivity Keeps Inflation Pinned

Ordinarily, rising wages are a concern for bond markets since it means there is a potential for wages to set off an inflationary spiral. Strong productivity keeps inflation fears in check since businesses will be able to produce more goods and services at lower unit costs (i.e. making more with less inputs). In addition, if productivity is rising, companies can afford to raise wages (household income) since the workforce is producing more for each hour worked. It also allows companies to hold off from raising prices since their cost per unit of output is falling.

If rising wages are accompanied with rising productivity, firms can pay higher wages without passing costs to consumers. For the policy makers at the US Federal Reserve, a strong US economy with rising productivity is the dream scenario since it makes it easier for the Federal Reserve to satisfy its dual mandate of promoting stable prices and maximum employment. Sometimes, the two goals are mutually exclusive.

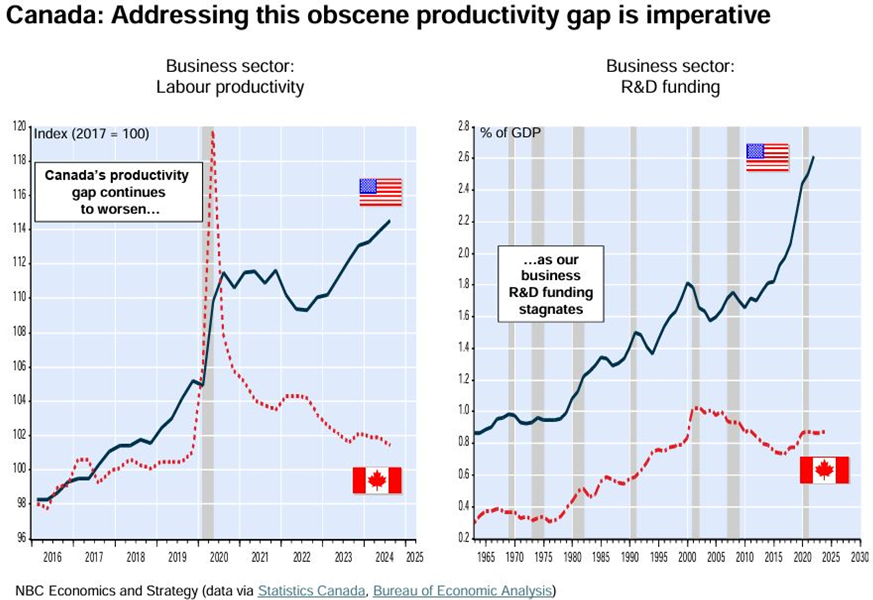

Canada’s Productivity Challenge

Canada’s productivity challenges stand in stark contrast to the United States. Unlike the Federal Reserve, which might be seeing its job made easier, the Bank of Canada has been sounding the alarm bells on Canada’s poor productivity growth. One of the main causes of this has been chronic under-investment in capital (machinery, equipment and technology). Canada has been investing far less per worker than other industrialized nations and this is seen in the amount of capital per worker; the oldest capital stock since data has been kept and slow investment in leading technologies. In the AI race, Canadian companies have been lagging significantly in deploying capital to harness potential benefits.

As noted above, Canada’s population had expanded far faster than peer industrialized nations. But without a productive way to employ that labor, those additional entrants to the labor force could not produce enough output to offset the rise in workers. As a result of poor productivity, Canada’s per capita income stagnated for over a decade – degrading Canadian living standards in a scene reminiscent of some of Europe’s slow-growth economies.

As noted in a previous edition of our newsletter, Canada is experiencing a population trap – something that has seldom been seen in a modern industrialized economy. A population trap occurs when the population of a nation rises faster than the economy’s ability to raise output, causing living standards to fall.

Limits & Debt Fears

In a perfect world, rising productivity in the US will help to make the economy grow faster, raise wages, keep inflation in check and help to lower interest rates.– an economist’s dream. Unfortunately, this perfect scenario is being offset by another issue that we have written about in previous issues of our newsletter – the rising tide of government debt which shows no signs of slowing down.

Across Europe, the combination of ageing societies, slow economic growth, high energy prices and rising defense spending commitments have combined to widen budget deficits. In Japan, newly elected Prime Minister, Sanae Takaichi has called an early election based on her promise to raise government spending and cut taxes on food. In Canada, the federal government and provinces are rapidly accumulating debt while economic growth inches along slowly. Meanwhile, the US shows little focus on getting its national debt down – despite rising tax revenue and select spending cuts lowering budget deficit estimates by $100 billion. While that is an extraordinary amount of money – the deficit will still add between $1.6 trillion and $1.8 trillion to the national debt in the current fiscal year.

Going somewhat unnoticed in recent months has been the trend of rising interest rates (yields) in the bond markets around the world. Japan’s 40-year government bond yield has reached a record high of 4.25%. US 30-year government bond yields are approaching very close to 5%. The benchmark 10-year US Treasury yield has been rising despite expectations for the US Federal Reserve to continue its policy of interest rate reductions. In France, the 30-year government bond yields have risen to 4.5% – the highest level since the 2011 sovereign debt crisis. Canadian government bond yields are lower than the nations noted above but are also trending upward toward 4%. .

Bond markets are signaling clear dissatisfaction with the lack of fiscal discipline. Investors are demanding a higher premium for two risks—one of which is relatively new for G7 economies. Bondholders require a “term premium” to compensate for lending over long periods, traditionally due to inflation risk eroding the value of future payments. Increasingly, however, investors are demanding an additional premium for lending to heavily indebted governments. Term premiums have been rising as investors confront debt‑to‑GDP ratios of nearly 240% in Japan, 136% in the U.S., and levels approaching or exceeding 100% across most major developed economies. The danger is that higher term premiums will push up borrowing costs for consumers and businesses, weighing on economic growth.

If the surge in U.S. productivity continues and helps power economic expansion, bond markets may stabilize and ease upward pressure on interest rates. A sustained productivity boom would help anchor inflation expectations and reduce the term premium. Even more helpful would be a meaningful slowdown in the growth of U.S. government spending.

It remains uncertain whether the U.S. productivity boom can be sustained, but there is reason for optimism. If U.S. policymakers want to support an economy that appears to be regaining momentum, they must demonstrate to bond markets that they recognize the fiscal challenge and are committed to reducing budget deficits. Doing so would lower the term premium on long‑term bonds, helping the economy further by reducing borrowing costs.