Gridlock Not Sidetracking Economy—So Far

With the first half of 2017 out of the way, investors are wrestling with mixed signals from the financial markets. Some fatigue seems to be setting in due to the state of politics in the US, Europe, and the leading economies of Latin America. In Asia, while there has been a steady build of concerns regarding China’s economy, it is North Korea that is garnering most of the headlines as its missile program alarms the world with the progress it has made. In this issue of our newsletter, we are taking a closer look at the potential for US political gridlock to impede the US economy’s growth trajectory and thereby begin to feed into market volatility.

US Economic Expansion Continues

The US economy continues to churn out a steady stream of jobs and concerns are building as to whether or not a labor shortage will develop that will ultimately fuel inflation. Many economists believe that the reason that interest rates are being raised at all relate to the Federal Reserve being preemptive rather than reactive to the potential for labor market strength to fire up inflationary pressures. Current data shows that the unemployment rate in the US sits at 4.4% – a 10 year low. At the state level, it has fallen below 3% for five states and 19 states have an unemployment rate between 3-4%.

Despite the good news on this and many other fronts, it is politics that is grabbing the headlines and erasing good economic news off of the front pages and nightly news. In the past, it has been said that Wall Street prefers political gridlock – which could be defined as the inability of the US Congress and President to sign bills into law.

It was thought that though the 2016 Presidential election was divisive, gridlock might be reduced during a Trump administration given that the Republican party controls the House, Senate, and the White House. Prior to the last election, gridlock was seen to be a characteristic of an Obama White House and Republican-controlled House and Senate. Barack Obama illustrated the level of gridlock he saw when he said, “If I sponsor a bill declaring apple pie American, it might fall victim to partisan politics.” While he was exaggerating, it about summed up much of his presidency.

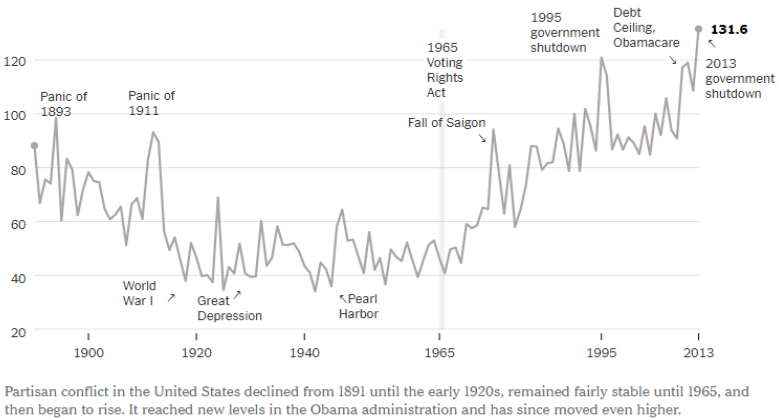

One of the few quantitative indicators that attempts to measure gridlock is the Partisan Conflict Index as calculated by the Philadelphia Federal Reserve. An analysis of this indicator in a recent edition of the NY Times looked at this index and according to its creator, Dr. Marina Azzimonti, “partisan conflict in the United States has reached an all-time high.” Figure 1 below shows this index over the long term. A further analysis of this data by Ned Davis Research shows that high readings in this index has coincided with an upwards trending market but low readings of partisan conflict have seen markets that rise at significantly lower rates. A recent note by Ned Davis on this topic was titled “Stock Market to Politicians: Keep Arguing.”

Figure 1: Historical Partisan Conflict Index

Source: NY Times, Marina Azzimonti, Stony Brook University. July 2017.

It may seem counterintuitive that elevated levels of partisan political conflict correspond with stronger stock markets. However, the data shows that markets have generally preferred gridlock as the chances of interventionist government policies being enacted decrease and therefore the chances of upsetting the proverbial applecart are reduced. Currently, markets appear content with a rate of economic growth that is not too fast and not too slow as it also allows interest rates to stay low and the unemployment rate continues to fall. In short, the stock market is saying that it likes the Goldilocks scenario of an economy that is neither too hot, nor too cold and prefers things to stay that way.

Gridlock: This Time Could Be Different

While history shows that gridlock has helped markets over time, this time we are concerned that the inability of the US government to agree on necessary fixes for tax reform, healthcare, and other structural challenges to the US economy could begin to result in a discount being applied to US equities over the longer term.

Healthcare spending accounts for about 17% of the US economy and all sides agree that some reform of Obamacare is needed to prevent the system from spiraling out of control. Despite numerous attempts at repealing and replacing Obamacare, the divisions within the Republican party are preventing legislation from being signed into law by the President. The Democrats say they will help to fix Obamacare but not repeal it. As serious as this issue is, it is also seen by some as a precursor to the probable failure of tax reform and infrastructure spending measures – both of which the markets were counting on as “done deals” until early February of this year.

We believe that unless things begin to turn soon, there is the potential for markets to begin to trim down future expectations of economic growth as stimulus and tax cutting measures are likely to be ground down in the legislative meat grinder. At this point, markets see little probability of any economic growth inducing measures making their way into law and have cut expectations for a pick up in the economy.

More Elections on the Horizon

Furthermore, the 2018 midterm elections are on the horizon and historically the party holding the White House tends to lose seats in the House of Representatives and Senate. According to the website insideelections.com, in the last 20 midterm elections, the party holding the White House has lost seats 18 times and has had an average loss of 33 seats. To put this in perspective, the Democrats need 24 seats to re-take the House majority in 2018. In the US Senate, the 2018 elections will see 34 seats up for grabs and 25 of these are Democrats, while 9 are Republican held. The Democrats would need to only pick up 3 more seats than they hold currently and they could take control of the Senate – further forcing the Trump White House to move to the political center or continue to choose to maintain gridlock. In short, all sides will have to engage in compromise to get things done.

Growth Duration Impressive But Weak

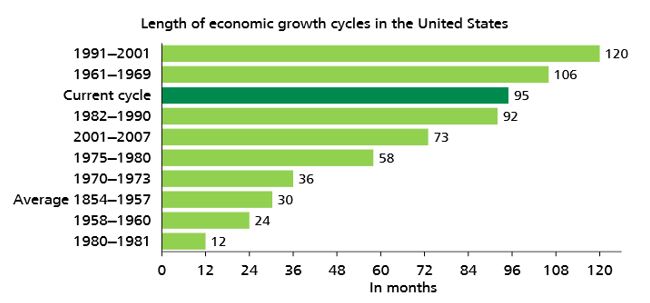

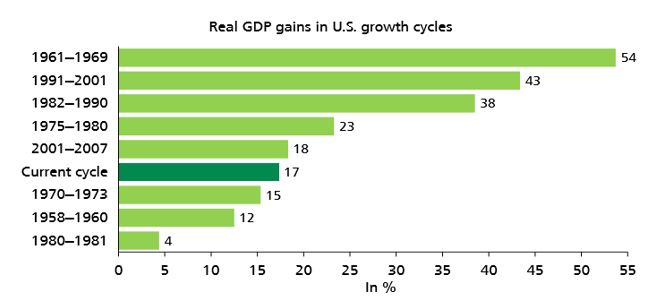

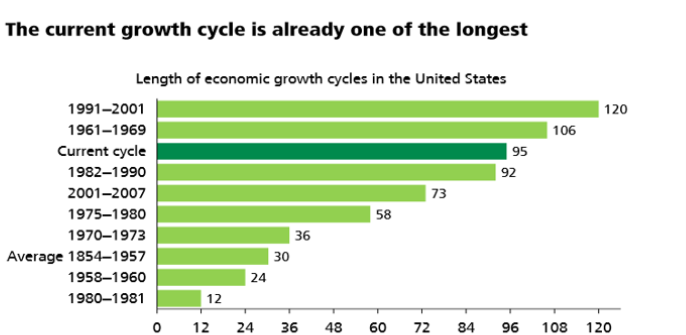

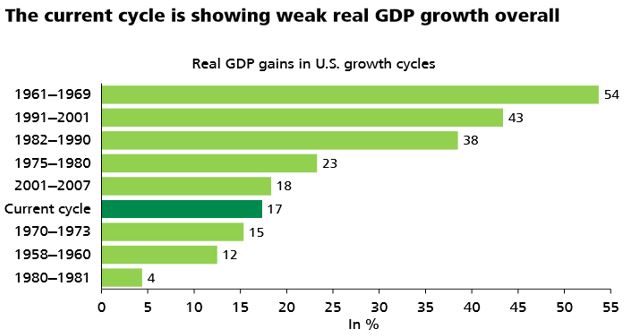

While we tend to agree with the role of gridlock in helping markets climb a wall of worry, we wonder if this time things are a little different (i.e. Could a little less gridlock be helpful over the long term?). As Figure 2 and 3 below show, the current economic cycle is one of the most unusual because it is currently the third longest US economic expansion on record but also one of the weakest—producing one of the lowest rate of economic growth on record. In the past, we have discussed the various constraints holding back the economy – some of which have not been seen before. These constraints include demographics (ageing societies); excessive debt (student, consumer, and government); poor productivity growth (producing more economic output with less capital and labor) and low business investment. Some studies have shown that businesses respond to gridlock and public policy uncertainty by restraining investment in new plants and equipment until they have greater clarity on how the rules will evolve.

Figure 2: The Current Growth Cycle is Already One of the Longest

Sources: National Bureau of Economic Research and Desjardins, Economic Studies. May 2017.

Figure 3: The Current Cycle is Showing Weak Real GDP Growth Overall

Sources: Datastream, National Bureau of Economic Research and Desjardins, Economic Studies. May 2017.

We have looked at each of these issues in past commentaries yet are surprised as how little has changed with each of these constraints and the underlying factors contributing to their lock on economic growth. In addition, we are surprised at how little has been put forward by any government anywhere as to how these issues can be addressed.

Even corporate America has begun to show its frustration and anxiety about political dysfunction holding back economic progress. Earlier this month, JP Morgan Chase CEO Jamie Dimon, widely regarded as one of the best bank executives in the world, told analysts on its most recent earnings conference call,

“Since the Great Recession, which is now 8 years old, we’ve been growing at 1.5 to 2 percent in spite of stupidity and political gridlock, because the American business sector is powerful and strong. What I’m saying is it would be much stronger growth had we made intelligent decisions and were there not gridlock. It’s unfortunate, but it’s hurting us, it’s hurting the body politic, it’s hurting the average American that we don’t have these right policies. So no, in spite of gridlock we’ll grow at maybe 1.5 or 2 percent. I don’t buy the argument that we’re relegated to this forever. We’re not.”

To be fair, Dimon is not the only corporate executive thinking along these lines. Stephen Schwarzman, CEO of private equity firm Blackstone Group, backed Dimon’s comments and stated that,

“At this point there are very few Americans that are very proud about the functioning of the US political system. I don’t know who the great booster is in terms of getting things done…I haven’t found anybody who thinks we’re batting 100 out of 100 in terms of how things are being handled.”

Looking at these comments from two of the most respected CEOs in the world, one would think that the financial markets are sure to run aground at some point. So far, markets have been able to continue rising and volatility is clinging to near historically low levels. This is in part because markets are focused on corporate earnings that are expected to reach record levels in Q2 2017 after nearly two years of being largely stagnant. The earnings rebound is being led by the energy, financials, and information technology sectors. According to data from S&P Capital IQ, operating earnings for the prior twelve-month period for the S&P 500 companies will be at an all time high of $123.61 – an increase of 1.5% from the previous quarter.

Global Economic Growth Finally Kicking In

It is also helpful that for the first time in nearly a decade, the economies of China, Canada, Japan, and Europe are growing faster than expected at the start of 2017 and globally, we are seeing the first hints of synchronized global growth. This is not to say that the global economy is booming but job growth is steady, unemployment is being trimmed back across most of the world, and trade is picking up—despite some protectionist sentiment rising within certain international trading relationships.

Given some of the economic data that we have seen in the last several months, this economic expansion might be nearing the record for longevity, but we believe it has some ways to go yet – gridlock or no gridlock. But markets should be careful to note that there is a difference between gridlock and dysfunction.

{kind=link}

{kind=link}