Global Markets Trying to Overcome Economic Challenges

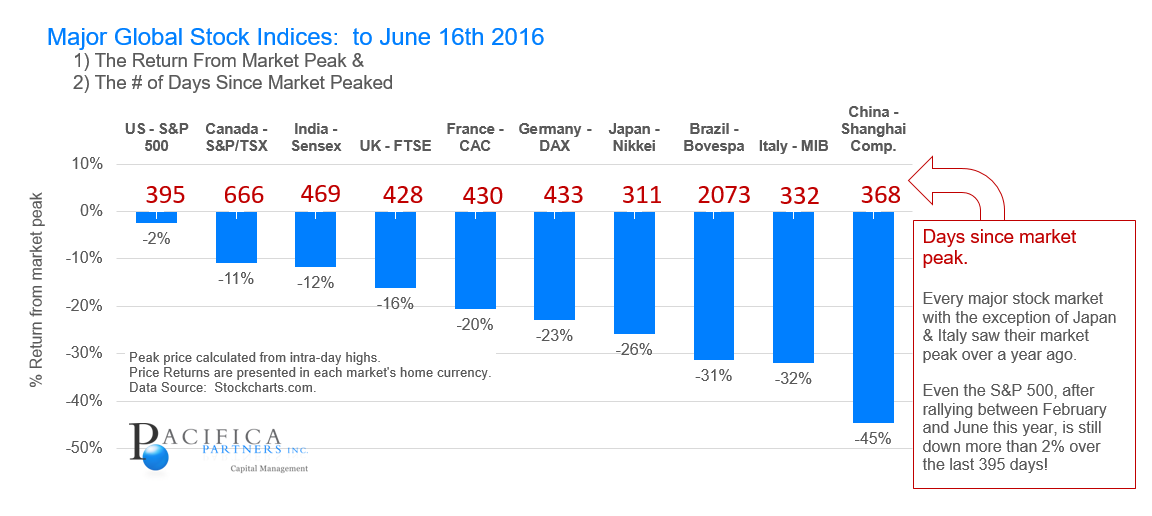

The chart below looks at the return of the stock markets from the ten largest economies in the world. It shows how far those markets have dropped from their prior high (peak level) and how long ago that peak was reached.

The data shows that the US equity market has been the most stable but the majority of global markets are in a bear market (one that is down 20% or more). It is somewhat surprising how little attention this fact gets in the media. Perhaps it is masked by the repeated down–up-down cycle of most major markets. However, it has been a long and protracted grind.

With that, the question then becomes “When will global markets begin to turn around again?” As always, that is a difficult question to answer. But what we do know is that globally the economy continues to be limping along. With slow economic growth and corporate profits in decline across most every industry, it is little wonder that markets are struggling.

As we have expressed in our newsletters in the past, the largest source of equity demand (buying power in the stock market) has been companies themselves buying back their own stock. Increasingly this is being done with borrowed money as corporate cash buffers have been running down. It is estimated that corporations are spending about 35-40% more than their cash inflows – and the difference is made up by borrowing. Markets are beginning to wonder “How long can this go on?”

As we have noted over the years, the impact of buybacks is to “artificially” increase the earnings per share (EPS) metric. However, this is masking the fact that overall profitability has been grinding lower and profit margins for most companies have already peaked and continue to grind lower. Simply put, companies need a stronger economy in which they can sell more of their goods and services. It really is that simple. If low interest rates are to have a stimulative effect on the economy and in turn help corporate profits grow, it has to come through increased corporate investment and government spending on infrastructure and other investments. If ever there was a time to lock in low borrowing costs, it is now. In Europe and Japan, governments are able to borrow at virtually no interest costs as government bonds are yielding a negative interest rate.

In our opinion, the benefits of low interest rates have long run their course and any further reductions in interest rates will actually have negative effects on the economy – many of which we have outlined in past commentaries.

As the chart shows, investors around the world are being confronted with challenging market conditions. Slowing earnings growth, peaking profit margins and sharply reduced corporate stock buyback activity are combining to put an anchor around global markets. In the past, whenever corporate profits slowed, the fix has come from some combination of easier monetary policy (not likely – since rates are about as low as they have ever been), government spending or rising productivity of capital and labor. (The latter is a challenge that we will discuss in our next blog or newsletter.) The best bet to strengthen the global economy is more government spending – but given political constraints this is a long shot for now. The G7 broached the topic at last month’s summit in Tokyo but no coordinated response was agreed to as most countries are worried about their debt levels – even at these incredibly low interest rates. The fix to the markets’ challenges needs to come from stronger economic growth and that is not going to be achieved through the magic of low or even negative interest rates.