DEBT: The Economic Challenge for the Next President

Shortly after winning the 1992 presidential election, some commentators said that the problems facing the country were so large that Bill Clinton might end up wishing he had lost. At the time, the US was facing a budget deficit of $450 billion which was about 4.5% of GDP and an economy feeling the effects of a recession. Measuring the deficit as a percentage of GDP is a good way of being able to see how big the shortfall is relative to the size of the economy (national income). If that seemed like trouble, when Barack Obama took the keys to the White House he faced a deficit approaching $1.4 trillion that tipped the scales at about 10% of GDP. In 2016, regardless of who becomes the next president, he or she could well be the first to have their hands tied by the national debt.

The 2016 election year certainly has been unique. Discussions of the challenges posed by the national debt used to be standard practice over the last several presidential cycles. This time, voters have focused their attention on other matters. Earlier this year, a Pew survey found that only about half of the US population considers it to be a priority- down from 72% in 2013. It is now number nine in terms of priorities the survey found. This is unfortunate because whatever complacency has been gained in recent years with respect to the national debt might not last. There are several reasons for this.

What Happens if Interest Rates Rise?

The national debt of the US sits at $19 trillion. Of this total, $14 trillion is owed to the public (non-US government holders of debt) and $5 trillion is known as intragovernmental debt (debt owed to entitlement programs such as Social Security and Medicare). Some commentators take issue with estimates that ignore the intragovernmental debt. This is money that at some point has to be paid into these programs to keep them solvent. The national debt has doubled in the last eight years while the economy has been turning in a disappointing rate of economic growth – despite ultra low interest rates. What has allowed the US to turn a blind eye to the dangers of the national debt is that low interest rates have eased the burden of carrying all of this debt. In short, even though the debt has doubled just during the terms of Barack Obama, interest payments have continued to fall such that they sit at only 1.25% of GDP. For comparison, interest payments on the debt were sitting at about 3.2% of GDP during the 1990 recession due to the higher interest rates prevailing at the time compared to today.

Of course, it cannot be assumed that low interest rates will last. If they do, it will only be because the economy continues to grind along at a slower for longer rate. But a slower economy comes with lower tax revenues .

In its Q3 2016 review, the non-partisan Congressional Budget Office (CBO) projected that rising obligations for social programs and interest payments on the debt would cause federal government spending to rise from 21% of the GDP in 2016 to 28% over the next 30 years. Their projections show that the annual budget deficit (which is added to the debt each year) would triple over the next 30 years. What matters is not the size of the debt but the ability to service it.

Troubling Trends

Recent data from the CBO shows that the budget deficit of the US has risen to $588 billion in the current fiscal year which is an increase of almost $150 billion higher than the previous year. Part of this unfavorable development is due to the fact that $39 billion of expenditures were moved into the 2016 budget on a one-time basis due to a quirk in the calendar).

But most troubling is that tax revenues generated by the economy are growing at less than 1% in 2016 but expenses are up by 5%. Furthermore, the CBO projections show that over the next several years, slowing population growth and more retiring workers will slow the increase in the US labor supply and begin to crimp economic growth. This will mean lower economic growth while the larger retiree population will increasingly draw upon entitlement programs.

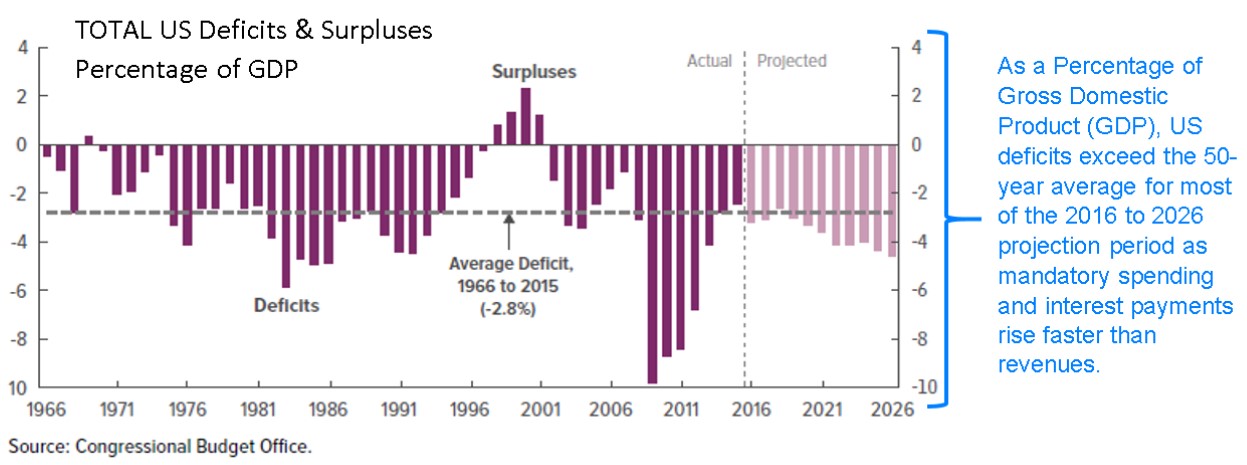

This is further quantified by the CBO. Their most recent projections show that the annual deficit will be $1.2 trillion in ten years and sit at 4.6% as a percent of GDP and will be “considerably larger relative to GDP than its average of the past 50 years”.

The Challenges Facing the Next President

Both candidates have laid out their campaign platforms for the polices that they will enact should they win the election. These priorities include more spending on infrastructure, defense and healthcare. But the next president of the United States will face a tough choice because his or her hands are going to be tied with respect to just how much budgetary maneuver room will be available.

When deficits get out of hand, there are only two options: cut spending or increase tax revenue. Given the slow rate of economic growth and rising costs of health care, cutting spending would hurt already slow rates of economic growth. If the rising budget deficits were to be covered by tax increases, then that too could have the reverse effect by hindering economic growth that depresses tax revenue. According to a 2010 paper by well known economists Christina and David Romer, a tax increase of 1% of GDP would reduce economic growth by about 3% over the next three-year period after the tax hike went into effect. Some tax increases and reform would be helpful but it is not a solution. The solution and therefore the challenge is getting an agreement on taxes and spending cuts.

Why Rising Deficits Matter

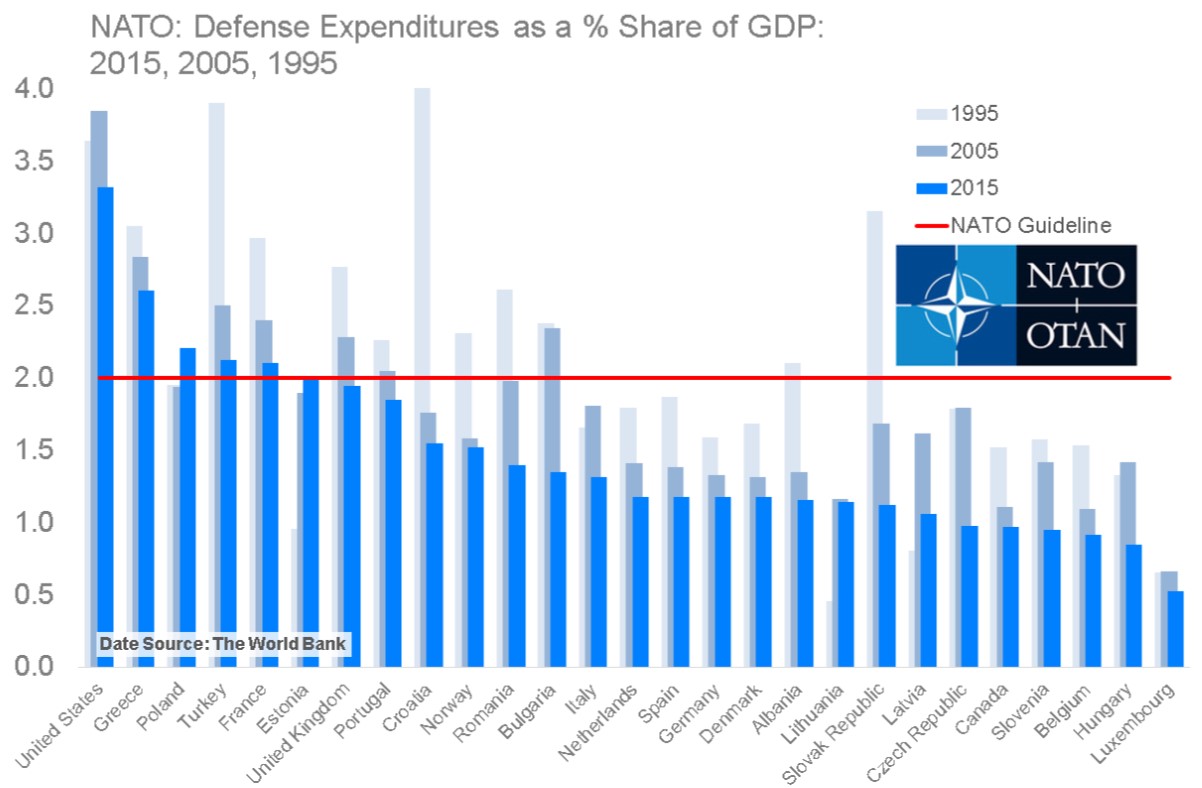

The reason that deficits matter is that they have the potential to begin consuming an ever increasing share of tax dollars and under the correct set of economic circumstances, the interest payments on the national debt will start to crowd out spending on traditional items in the budget. One item in the budget that is of special interest to many observers is defense spending. Currently, the US defense budget exceeds that of the next ten nations combined. The problem is that geopolitical challenges have risen and whether it is Russia, China or the Middle East – the US is likely going to choose to raise its defense spending. As the NATO Secretary General Jens Stoltenberg told a summit gathering earlier this year that “The world is a more dangerous place than just a few years ago.” To underline the status of NATO member contributions to defense spending, the graph above shows that Greece is the second biggest spender in NATO on defense when measured as a share of GDP. If it is any nation that was entitled to a pass on meeting its NATO commitments, it should have been Greece given that its economy shrank by over 25% in recent years!

For the first time in many years, the US role in the future of NATO has been discussed by the candidates and has become a political issue. NATO rules say that each nation should spend an equivalent of 2% of GDP on their respective defense expenditures. NATO’s own data shows that US defense spending has fallen $757 billion in 2009 to $664 billion in 2016 (a decline of 12%).

In future years, the ability of the US to continue to subsidize the lack of defense spending by nations such as Canada, France and Spain will be challenged by its fiscal constraints. Other nations face similar fiscal constraints. That being said, defense spending is more likely to rise than fall given the geopolitical challenges that prevail across the world.

Infrastructure Spending

While there seems to be broad political consensus amongst the candidates for the need for increased spending on infrastructure for new highways, bridges and airports it is likely that budgetary realities could reduce the scale of such spending programs. Such a program is needed to replace aging infrastructure and would be hugely stimulative to the economy but once again, the debt begins to limit flexibility and choice.

The scare scenario around the debt revolves around what would happen in the event of a recession. During a recession, economic activity drops and along with it—income. In turn, so does tax revenue that flows to the government. Given that the national debt is going to hit the $20 trillion level sometime in 2017, any decline in tax revenue from a recession would cause a severe expansion in the budget deficit.

Debt is a Hibernating Bear

While the national debt has slipped off of the front pages for now, it is not likely to remain a non-issue forever. By 2020, the CBO expects that all of the tax revenue collected by the US government will only be enough to cover spending on social security, healthcare and interest on the debt. All other spending would have to be covered by borrowing. It is under this sort of scenario where the national debt will be a challenge for the US government. Hopefully, long before this scenario gets to the nightmare level meaningful reforms to entitlement programs will be made. So far, it seems that the era of ultra low interest rates had provided an opportunity for dealing with the national debt. Unfortunately, the opportunity to begin to fix it has thus far been wasted. A shock to the economy that slows the economy will certainly reawaken the debt bear.

Gauging Potential Market Impact

There is often a great deal of effort expended on trying to figure out which party’s policies will be “better for the market”. We are always cautious around this sort of talk because markets tend to be pretty good at figuring out these outcomes well in advance of the actual outcome. Yet they can still be surprised as we witnessed in the UK’s Brexit referendum in June of this year. As we have touched on above, we believe that the economic policies of the next US President will be impacted by the path of the global economy and the constraints of the national debt. We believe that there is little to be gained in trying to predict an outcome and pre-positioning one way or another. The best strategy is much less dramatic and instead involves waiting to capture any opportunities that arise from any potential mispricing in the election aftermath.