Eyes on Hormuz: Energy Markets at a Geopolitical Crossroads

In This Issue:

- Early rout of Iranian military offset by Iranian shutdown of Strait of Hormuz

- Hormuz closure has halted oil, LNG and fertilizer exports from the Middle East

- Reordering of global energy supply

- Economic implications of Epic Fury

The most recent crisis in the Middle East involving Iran and the US-Israel joint strike has reminded the world once again that global energy supplies are still the lifeblood of the world economy; when they are threatened or restricted the economic impact is quickly felt. As was the case when conflict between Russia and Ukraine escalated in February 2022, energy prices and threats to fertilizer supplies became entrenched sources of economic angst. Once the US and Israel launched Operation Epic Fury, the military route of Iranian military capacity was quick. But Iran responded with a powerful example of asymmetric warfare. With its limited ability to match the US and Israel, it resorted to the use of low-cost, unconventional and very disruptive tactics using drones, mines and the closing of the Strait of Hormuz to inflict an economic cost.

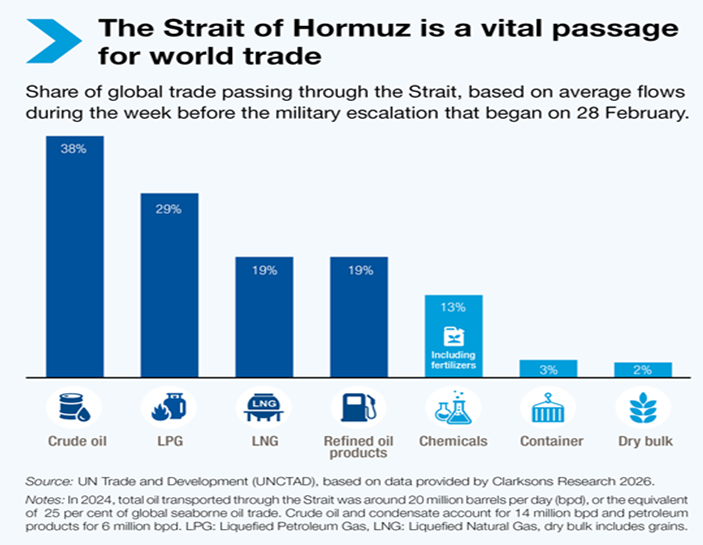

In 2024, our first quarter newsletter looked at naval chokepoints that posed a risk to global trade and energy flows. Along with the Panama, Suez Canals, and other maritime chokepoints, the Strait of Hormuz was highlighted. Prior to Epic Fury, the Strait of Hormuz saw 20 million barrels of crude and refined oil products flow through it each day. This figure consisted of 15 million barrels of crude oil and nearly 5 million barrels per day of petroleum products, such as diesel, jet fuel, gasoline, and other refined products. In total, the Strait of Hormuz sees about 25% of all global flows of seaborne oil and 20% of total daily consumption flow through its narrow waterway. The UN Trade and Development organization (UNCTAD) estimated that in the week prior to military escalation, the month of February ended with a surge in exports from the region that saw the Strait of Hormuz’s share of crude oil exports surge to 38% of global seaborne oil movement.

In addition to crude oil, the Strait of Hormuz is an important transit corridor for liquefied natural gas (LNG) which is the second most valuable export after crude oil. About 20% of global LNG trade passes through it with nearly all of this belonging to Qatar and a small amount to the United Arab Emirates (UAE). It is the nations of Asia that are impacted by the LNG flows since over 80% of the LNG from the region goes to its energy thirsty nations. In particular, three nations – India, China, and South Korea – receive more than half of this supply.

If the energy exports were not significant enough – the world has come to also appreciate the fact that the Strait of Hormuz is also a significant conduit for the export of fertilizer inputs and outputs. About one-third of the world’s fertilizer ingredients move through the Strait.

Closing of the Strait of Hormuz

Knowing it could not match the military power of the US and Israel, Iran responded with missile attacks of its own. But as this capacity was diminished as the conflict went on – Iran closed the Strait of Hormuz. Shipping had fallen dramatically and the number of cargo ships moving through the Strait went from 103 vessels in the last week of February to a small handful within weeks. The net impact was to effectively close the strait and energy exports fell.

In addition to the closing of the Strait, military counterattacks from Iran have significant diminished the region’s LNG capacity. Qatar—the world’s largest LNG exporter—has been forced to halt production after direct strikes on its key LNG production facilities. Qatar has been forced to declare force majeure on its long-term contracts which allows it to suspend or delay its delivery owed under its LNG export contracts. Middle Eastern LNG exports have collapsed by roughly 70%, removing nearly 20% of global LNG supply overnight. This sudden loss of volume has tightened markets across Europe and Asia, driven benchmark prices sharply higher, and exposed the vulnerability of global gas supply chains to chokepoint disruptions. The scale and speed of this shock exceed even the post Ukraine gas crisis, underscoring how critical the Strait remains to global energy security.

As spot prices of LNG surged and export quantities evaporated from the region, countries across Asia have turned back to coal to maintain electricity supply, lifting coal plant output caps, boosting imports, and accelerating fuel switching to avoid blackouts. This rapid return to coal underscores the fragility of global gas supply chains and highlights how chokepoint disruptions can reverse years of progress toward cleaner energy.

Reordering of Global Energy Supply

The threat that Iran could close the Strait of Hormuz has weighed on energy markets for over three decades and today, that threat has become a reality. To help calm oil markets, the industrialized nations agreed to release 400 million barrels of oil from global strategic petroleum reserves. The markets greeted this policy with a yawn for two reasons – this is about 20 days of crude supply that goes through the Strait of Hormuz and given constraints – it would take about 200 days to get that amount of oil from reserves to the market.

Asia is the most dependent continent on oil from the Middle East. Japan receives 95% of its crude imports from the region; South Korea at about 75%; India at 55% and China at 50%. Taken together, this leaves Asia meeting about 60% of its crude oil needs from the Middle East.

When it comes to natural gas (LNG), 90% of Middle Eastern LNG is exported to Asia. India is the most dependent on the Middle East as about two-thirds of its needs come from Qatar. Due to Iranian attacks that destroyed 17% of its LNG export capacity, Qatar has declared force majeure which is the exercising of a clause that allows a supplier to suspend or delay delivery obligations due to extraordinary events. The repairs on Qatar’s infrastructure for the export of LNG will take 3 to 5 years to complete.

According to Henning Gloystein, managing director for energy at political research firm Eurasia Group, there will be reduced LNG supplies for the balance of this decade. Gloystein further stated that “Anybody at the moment who is in a country or a company that has plans to do gas-fired power stations is going to have to review these. There is going to be no return to normal even if the war ends.”

At this point, it is expected that even with a permanent end to the conflict, the return of oil and LNG flows from the region to pre-war levels would take several months and move forward at an uneven pace. Clearing the current queue of ships in the Persian Gulf alone would require about two weeks if the strait were fully open – which is not yet the case. Tanker movements would also lag because of port damage, sunken vessels, elevated war-risk insurance, and the need for sustained security. Repairs to loading equipment and port infrastructure could take months rather than weeks. Production recovery could then take three to four months even under immediate peace, and very likely much longer, given that prolonged shut-ins of energy production sites materially increase the risk of restart complications.

Coal – The Other Energy Shock

For many years, climate treaty negotiators from many nations have tried to move the world away from coal – often referred to as the dirtiest fossil fuel. Rising energy demand in the developing world made this task difficult even under the best of circumstances but progress was being made. One outcome of this war is likely to be the fact that many nations will have to consider the trade-off between cleaner burning LNG against the security provided by domestic sources of coal. Already, the Iran War has triggered the largest rebound in coal demand in more than a decade.

Some nations in Asia have switched back to coal to replace the missing LNG supplies they are no longer receiving. South Korea has been one of the most aggressive nations in making the switch back to coal as it lifted the output caps on coal-fired power plants by allowing them to run at full capacity. According to consulting firm Wood MacKenzie, the switch to coal will allow South Korea to meet its summer needs for more energy while it awaits for LNG to begin flowing out of the Middle East.

Japan has also switched to the aggressive use of coal as it will offset up to 70% of its natural gas fired power generation capacity. For its part, India’s government has ordered all coal plants to operate at full capacity for the summer the second quarter of the year while China will make use of its newly built record coal-power capacity by utilizing its large domestic coal reserves. Even Europe is not able to withstand the pressures to maintain a steady supply of energy for its nations. Coal usage has risen in Europe. Germany – which led the fight against carbon emissions in Europe for years – is now considering the reactivation of mothballed coal plants to curb electricity prices.

Implications Beyond Energy

The consequences of the war – apart from the human and environmental impact – are being felt beyond energy prices. Oil and gas are also the inputs for thousands of products such as fertilizers, plastics, carpets, solvents and pharmaceuticals. Petroleum industry sources have often cited the importance of their industry by stating that over 2000 products are derived from hydrocarbons.

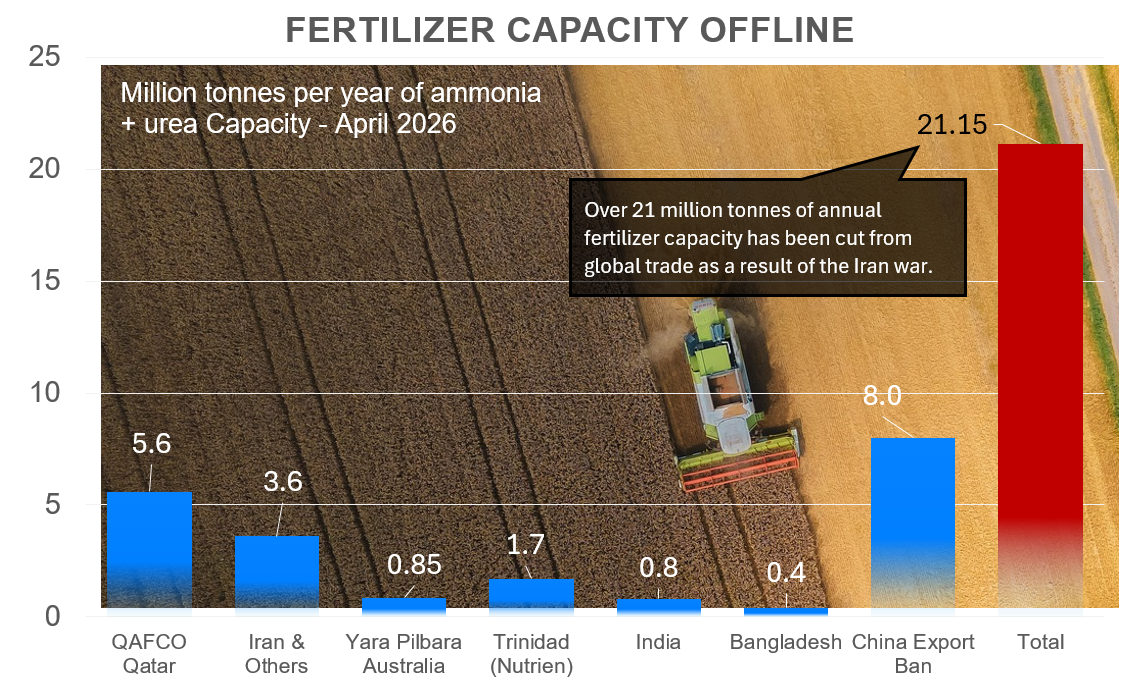

While the potential impact on any industry is sure to be sharp, policymakers and financial markets are keenly watching for the impact on the agricultural industry. Fertilizer production relies on natural gas because it is both the chemical feedstock and the energy source required to make ammonia—the foundation of all nitrogen fertilizers. Without natural gas, the modern fertilizer industry would not exist. It is worth noting that fertilizer production has undergone three shocks since 2020 – the COVID pandemic; and the invasion of Ukraine and the current conflict in Iran.

The rapid halt to the export of natural gas from the Middle East due to the closure of the Strait of Hormuz has put the global fertilizer industry on edge. Fertilizer is a significant cost for farmers and a sharp rise in input costs for farmers will eventually lead to higher food prices and broadening of inflation pressures. One mitigating factor for now is that demand for fertilizer at this time of year is uneven because the Northern Hemisphere is preparing fields for planting and the Southern Hemisphere is harvesting which means fertilizer demand in the Southern Hemisphere is currently low. Fortunately, the main destination for Middle East exports of fertilizer and related inputs such as LNG for fertilizer production is the developing nations of the Southern Hemisphere. Still, the impact is being felt in North America as a survey by the American Farm Bureau Federation showed 70% of 5700 famers surveyed said they cannot afford all of their fertilizer needs this year.

All nations have a vested interest in restraining food price inflation since it leads to instability in developing nations and angry voters in developed nations. It is one of the reasons that international sanctions against Russia largely exempt its fertilizer exports with Western nations being important markets despite the rivalries over Ukraine. Europe still continues to import over 20% of Russian natural gas exports for its energy and fertilizer needs. This highlights the structural importance of natural gas in global food supply and the complications that exist when sanctions are levied against a nation that is an important part of the global fertilizer and natural gas supply.

Markets Looking to War’s End

Global energy markets will remain structurally tighter, more volatile, and more politically fragmented long after the Iran War ends. The conflict has disrupted physical supply routes, damaged critical infrastructure, and accelerated a global rethink of energy security, all of which create lasting aftershocks. It will take years of rebuilding infrastructure in the Middle East before pre-war levels are once again reached. Export terminals, gas fields and equipment have been destroyed. The world’s spare capacity in energy infrastructure has been diminished at a time that global oil demand was already straining the ability of the energy producers to supply it.

History shows that wars end when one or both sides have exhausted themselves or the costs are too high to continue. For the Iranian side, the focus is going to eventually return to the need to rebuild and stabilize the government and for the US, it is a midterm election year and politicians know voters are feeling the pinch at the gas station and grocery store. For financial markets, thus far – they seem to be pricing in a scenario that negotiations will eventually succeed or if they do not – going forward, the war will transition to a slow but steady fade.